Understanding Income Tax — Junior Cycle Maths Applied Arithmetic

Income tax is one of the most practical topics in Junior Cycle maths. The calculation follows a clear sequence: start with gross income, calculate gross tax, subtract tax credits, then deduct PRSI and USC to arrive at your take-home pay. This post walks through each step.

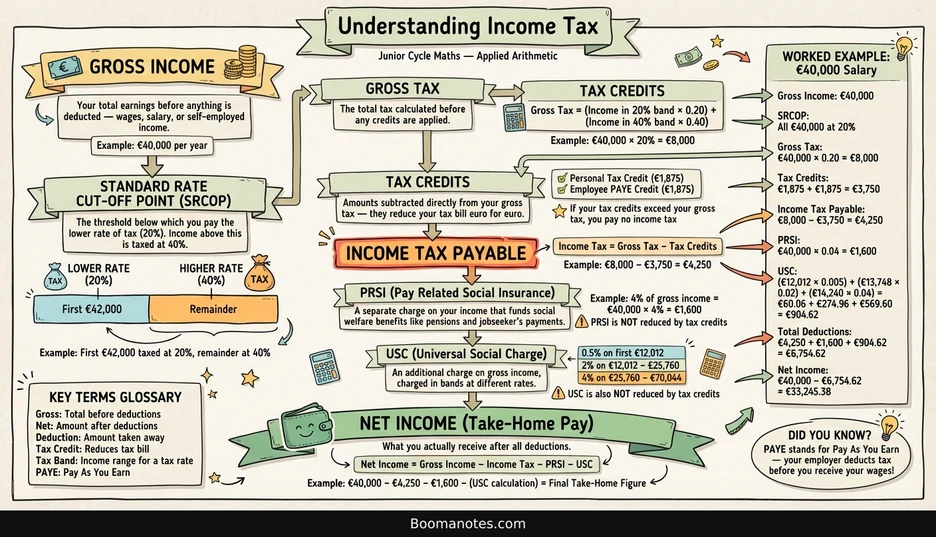

Step 1 — Gross Income

Gross income is your total earnings before anything is deducted — wages, salary, or self-employed income.

Example: A person earns a salary of €40,000 per year. Their gross income is €40,000.

Step 2 — Tax Bands and the Standard Rate Cut-Off Point (SRCOP)

Income tax in Ireland is charged at two rates:

- 20% (standard rate) on income up to the Standard Rate Cut-Off Point

- 40% (higher rate) on any income above that threshold

The SRCOP varies depending on personal circumstances. For exam purposes, you’ll be given the cut-off point in the question.

Example: If the SRCOP is €42,000 and you earn €40,000, all your income falls in the 20% band. If you earned €50,000, the first €42,000 would be taxed at 20% and the remaining €8,000 at 40%.

Step 3 — Gross Tax

Gross tax is the total tax calculated before any credits are applied.

Gross Tax = (Income in 20% band × 0.20) + (Income in 40% band × 0.40)

Example (€40,000 salary, SRCOP of €42,000):

All €40,000 is within the 20% band:

€40,000 × 0.20 = €8,000 gross tax

Step 4 — Tax Credits

Tax credits are amounts subtracted directly from your gross tax — they reduce the tax bill euro for euro. Common tax credits include:

- Personal Tax Credit: €1,875

- Employee PAYE Credit: €1,875

If your tax credits exceed your gross tax, you pay no income tax (but you don’t get a refund of the difference).

Example: Total tax credits = €1,875 + €1,875 = €3,750

Step 5 — Income Tax Payable

Income Tax Payable = Gross Tax − Tax Credits

Example: €8,000 − €3,750 = €4,250 income tax payable

Step 6 — PRSI (Pay Related Social Insurance)

PRSI is a separate charge on your income that funds social welfare benefits like pensions and jobseeker’s payments. It is not reduced by tax credits.

The standard employee rate is 4% of gross income.

Example: €40,000 × 0.04 = €1,600

Step 7 — USC (Universal Social Charge)

USC is an additional charge on gross income. It is also not reduced by tax credits. USC is charged in bands:

| Band | Rate |

|---|---|

| First €12,012 | 0.5% |

| €12,012 to €25,760 | 2% |

| €25,760 to €70,044 | 4% |

Example (€40,000 salary):

- €12,012 × 0.005 = €60.06

- (€25,760 − €12,012) × 0.02 = €13,748 × 0.02 = €274.96

- (€40,000 − €25,760) × 0.04 = €14,240 × 0.04 = €569.60

Total USC = €60.06 + €274.96 + €569.60 = €904.62

Step 8 — Net Income (Take-Home Pay)

Net income is what you actually receive after all deductions.

Net Income = Gross Income − Income Tax − PRSI − USC

Example: €40,000 − €4,250 − €1,600 − €904.62 = €33,245.38

Full Worked Example Summary

| Step | Calculation | Amount |

|---|---|---|

| Gross Income | Salary | €40,000 |

| Gross Tax | €40,000 × 20% | €8,000 |

| Tax Credits | €1,875 + €1,875 | −€3,750 |

| Income Tax | €8,000 − €3,750 | €4,250 |

| PRSI | €40,000 × 4% | €1,600 |

| USC | Banded calculation | €904.62 |

| Total Deductions | €4,250 + €1,600 + €904.62 | €6,754.62 |

| Net Income | €40,000 − €6,754.62 | €33,245.38 |

Key Terms Glossary

- Gross — Total before deductions

- Net — Amount after deductions

- Deduction — Amount taken away

- Tax Credit — Reduces your tax bill directly

- Tax Band — Income range for a tax rate

- PAYE — Pay As You Earn (your employer deducts tax from your wages before you receive them)

Practice Questions

- A person earns €35,000 per year. The SRCOP is €42,000. Calculate their gross tax.

- Using the same salary, subtract tax credits of €3,750 to find the income tax payable.

- Calculate the PRSI at 4% on a salary of €50,000.

- A person earns €30,000. Calculate their total USC using the bands above.

- Putting it all together: find the net income for a salary of €45,000 with an SRCOP of €42,000, tax credits of €3,750, PRSI at 4%, and USC as per the bands above.

This post is based on an AI-generated infographic from Boomanotes — turn any study notes into visual revision aids.